“If a thousand men were not to pay their tax-bills this year, that would not be a violent and bloody measure, as it would be to pay them.”

~ Henry David Thoreau, Civil Disobedience.

Civil Disobedience is a seminal text. That, I hope, is self-evident. Whoever you might call a revolutionary since 1884 has been forced to read it. Some have fallen in love with it for its civility and mantras of peace. Others will forever hold a grudge against Thoreau for his dogged commitment to peace. Either way, Thoreau’s solution was born of an inability to enact direct change in the pieces of paper that ruled the world he inhabited. The poll tax was there long before Thoreau saw his disagreements with slavery or the American-Mexican war. His disobedience was an act born of politics rather than the chilling cold of starvation. There was no need to light a fire to stay alive. As such, even the most fearsome revolutionary can forgive him for his reluctance. The fire needs petrol. It needs a hunger, an anger.

When the 2024 Finance Bill is mentioned, the first reaction is often of disgust and anger. Anything else would be absurd. How could the Bill that led to June 25th, and the seven days of chaos, be forgotten? The 16% tax on bread, imported eggs, onions, potatoes. The 2.5% tax on motor vehicle ownership. Some aspects of the Bill, it seems, are forgotten. The 6% “significant economic presence tax” that would have forced Bolt and Uber to pay taxes in Kenya – good or bad depending on who you ask or where you sit or stand.

The Bill was a failure: the protests showed as much. Rejected, even when it was amended. It is possible to tease out some nuance in it as legislation, but to say that it was salvageable would be a blatant lie. A shame, for the justification for the Bill was noble. Raise money to deal with national debt.

The number will keep going up, the price may never be paid. I have said before, it is not my space to speak on Kenyan politics. It is not my place to give suggestions on policy. I can, however, explain what little there was in the Bill, and what there was not. The omissions will always be of more interest.

The discussions being had around tax across the world are also of interest when seen alongside the Bill that was doomed to fail. Below is a quick summary of the Bill’s main taxation changes, post amendment. Naturally, some of the more granular changes are omitted. This article focuses on the highlighted taxes. Later editions in this series will look at the more complex excise duties and general taxes.

| Tax/Levy | Rate/Change | Type |

| Significant Economic Presence Tax | 30% of deemed taxable profit (based on 20% of turnover) | % |

| Minimum Top-Up Tax | Ensures at least 15% effective tax rate | % |

| Motor Vehicle Tax | 2.5% of vehicle value (min KSh 5,000, max KSh 100,000) | % + Fixed |

| Capital Gains Tax | 15% final tax (5% if ≥ KSh 3B invested & held ≥ 5 years) | % |

| Excise Duty on money transfer services | Increased from 15% → 20% | % |

| Excise Duty – Beer/Wine | KSh. 22.50 per cl pure alcohol | Fixed |

| Excise Duty – Spirits | KSh. 16 per cl pure alcohol | Fixed |

| Excise Duty – Cigarettes (filtered/plain) | KSh. 4,100 per mille | Fixed |

| Excise Duty – Nicotine products (non-combustion) | KSh. 2,000 per kg | Fixed |

| Excise Duty – Liquid nicotine (e-cigarettes) | KSh. 100 per ml | Fixed |

| Excise Duty – Coal | 5% of value or KSh 27,000 per ton (whichever higher) | % + Fixed |

| Excise Duty – Vegetable oils | 25% | % |

| Excise Duty – Advertising (internet, social media) | Increased from 15% → 20% | % |

| Miscellaneous Fees – Import Declaration Fee (IDF) | Increased from 2.5% → 3% | % |

| Export & Investment Promotion Levy | 3%–20% depending on goods (e.g., 20% on leather/footwear, 10% on clinker, 3% on motorcycles/furniture) | % |

| Eco Levy (electronics, IT equipment, smartphones, etc.) | Shs. 98–225 per unit (variable based on product classification) | Fixed |

| Bread (VAT) | 16% (was exempt) | % |

| Insurance Premiums (VAT) | 16% (was exempt) | % |

| Betting and Gaming (VAT) | 16% (was exempt) | % |

| Pest Control Products (VAT) | 16% (was exempt) | % |

| Electric Bicycles (VAT) | 16% (was exempt) | % |

| Sanitary Towels and Tampons (VAT) | 16% (was exempt) | % |

| Agricultural Sprayers and Equipment (VAT) | 16% (was exempt) | % |

| Financial Services – Digital (VAT) | 16% (was exempt) | % |

| Solar Equipment (VAT) | 16% (was zero-rated) | % |

| Water Treatment Chemicals (VAT) | 16% (was exempt) | % |

| Medical Supplies – Diagnostic Kits (VAT) | 16% (was exempt) | % |

| Education Materials – Textbooks (VAT) | 16% (was exempt) | % |

Of course, it is worth recognising that this is only an exhaustive list of tax changes. It does not take into account administrative changes. For example, the effects of raising the VAT registration threshold from KSh 5,000,000 to KSh 8,000,000, thereby decreasing the number of smaller businesses that will reclaim the VAT on their products through the input/output system, are not analysed. Regardless, the sea of petrol, of pulverised sixteen-percenters and the anger of a people, is of great interest. Such seas should be carefully examined.

A Quick Dip Into the World of Economics

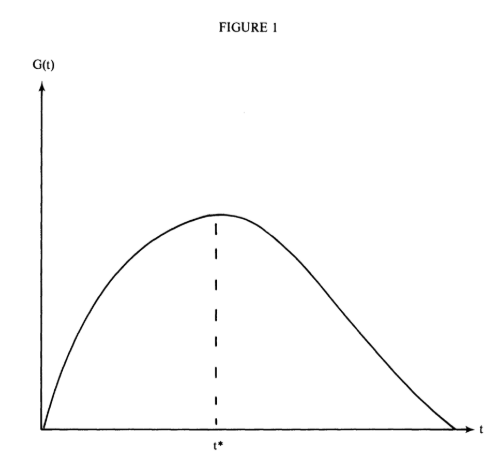

Behold, the Laffer Curve.

The x-axis is the rate of taxation from 0% to 100%, and the y-axis is the revenue of the government from the scheme. Traditionally, this is applied to income tax since it is an easy tax to apply and monitor. The argument is as follows:

- When the government does not tax, it makes no revenue from tax.

- When the government taxes everything, why would anybody go to work? If they did, they would have to break the law to earn any money. Some undoubtedly do this, and many just do not work. The government makes no money from the tax either way.

- As such, the ideal rate of taxation for maximising government revenue is somewhere between 100% and 0%, with revenue decreasing with the rate moving in either direction.

The complex ways in which the said rate changes is a point of endless argumentation among economists. The curve does not tell you the magical Laffer Point, the point of maximum revenue. There could be multiple optimal taxation rates. There may be a sharp drop after a certain rate, or a massive peak across an entire range. Income tax is a complex phenomenon, but the graph should suffice to visualise the concept. Naturally, the idea also carries over to other forms of taxation.

Now, the Laffer Curve has many flaws. In fact, it should probably not even be called the Laffer curve. Jules Dupuit wrote of an identical modeling of taxation in 1884, and Edmund Burke argued about a similar issue in the English Parliament of 1774. Such things may be endlessly debated. The question remains, were the Kenyan tax proposals of June 2024 obviously flawed in their economics?

16% On Life

Alan Blinder made an astute observation about the Laffer point for sales taxes. When a market can be quickly abandoned, the Laffer point comes much earlier than for staple, necessary markets. A 16% tax on solely Vanilla yoghurt would lead to little revenue, since people are likely to start getting Vanilla icecream or strawberry yoghurt instead of the now more expensive Vanilla yoghurt. A tax on bread, however, is quite difficult to escape. Buying flour and baking bread at home may end up costing as much as the bread from Carrefour, while taking more time and energy.

These broad taxes are highly unlikely to go past a Laffer point, since the tax can simply be raised because there is little way to avoid a tax on the purchase of bread. As such, a Lafferian analysis would be that taxing bread was a perfect move to raise money. It may go so far as to say that removing other taxes in favour of a higher bread tax would be the best move.

Of course, such analysis ignores the increase in hunger rates across the country. It is about maximising taxation, why should hunger rates be of significance? Perhaps eventually the problem is bad enough that the analysis needs to acknowledge the trade-offs of a decreasing population leading to less people to buy bread and pay the bread tax.

Such great gains are also to be found in taxing the necessities of life. Insurance, sanitary products, financial services, medical supplies, and educational materials are central necessities for individuals across the country. Sometimes, purchasing them is even mandated by law. Car insurance and school attendance (educational materials) for example. The tax must be paid, the rate can be raised. The Laffer point will not be hit until the population decrease is enough to warrant a decrease in the rate. Until then, party on!

16% On Competition

Other taxes seem to be protectionist of all pre-existing large businesses. Kenchic and Brookside are unlikely to face major issues with a 16% VAT on agricultural equipment and pest control products. Perhaps they pay a little more when one of their many hundred machines needs replacing, or a little more on pesticides. However, the lone farmer in Kiambu trying to increase the size of his farm must now raise more money to buy sprayers and processors, and a 16% increase in the cost of his pesticides is likely to put more strain on him than it does a larger business. Competition is restricted locally as well as externally. Similar provisions are evident with VAT on water treatment chemicals. These taxes will have maximal impact on up-and-coming businesses, thereby protecting pre-existing giants..

16% On That Other Stuff

The 16% VAT on solar equipment was also widely spoken of (Abdullah Ajibade). Its impacts would have been counterproductive to the various “eco taxes” that were mentioned as a benefit of the tax. What environmental gain is there from taxing the sale of devices while also making solar power more expensive? There was also astute analysis from the taxi driver who took me home today. Solar power means not paying KPLC for your electricity. One could call it protectionism.

There are also taxes which frankly do not need further analysis. A 16% VAT on electric bicycles, while high, merely raises their price for the small minority that may buy them. The same can be said for the new VAT on Betting and Gaming.

To Conclude

The 16% VATs are not malicious. To say such a thing would give life and soul to what is ultimately a cold piece of paper. It has no feelings, it has no aims in itself. It is merely the result of cold, bureaucratic engineering, designed to appease the largest number of powerful trusts.

However, policy should not be solely economic. The Bill’s failings rest precisely in this misunderstanding of what taxes are for. They are not, contrary to belief, solely about making money. They are the true central policy of any government, senior even to legal matters. When no consideration is given to their human impact, the results are evident for all those with eyes to see.

The cold bill then became nothing more than fuel for a parliamentary fire of hunger and anger.

Works Cited

Ajibade, A. (2024, June 21). Kenya Finance Bill 2024 passes second reading amid public outcry. Techpoint Africa. https://techpoint.africa/news/kenya-finance-bill-second-reading-amid-public-outcry/

Blinder, A. S. (1981). Thoughts on the Laffer curve. In L. H. Meyer (Ed.), The supply-side effects of economic policy (pp. 81–93). Kluwer-Nijhoff Publishing.

EY Global. (2024). Kenya proposes tax changes under the Finance Bill, 2024. EY. https://www.ey.com/en_gl/technical/tax-alerts/kenya-proposes-tax-changes-under-the-finance-bill–2024

National Council for Law Reporting (Kenya Law). (2024). Value Added Tax Act. Kenya Law. https://new.kenyalaw.org/akn/ke/act/2013/35/eng@2024-04-26

Parliament of Kenya. (2024, May 9). The Finance Bill (p. 30). The Government Printer.

Post Script

The story of the 2024 Finance Bill is not yet over. The petrol has been chemically sampled and analysed, but petrol alone does not make a fire last and burn. A proper fire needs wood to hold its heat and keep it fed across the coldest nights. The wood shall be inspected in a later work.